Analyzing Udemy’s IPO Filing: $430M Revenue; $30M CorpU Acquisition; Consumer Segment Stalls, Enterprise Grows

Udemy is going public. Its IPO prospectus gives us a rare opportunity to take a peek into the business.

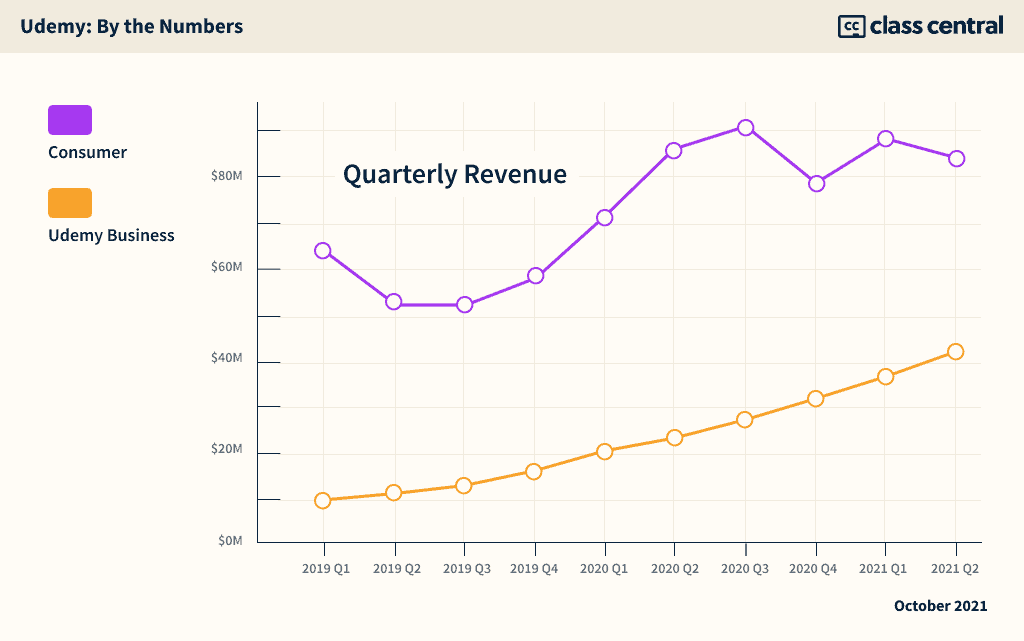

- Udemy’s revenue increased to $429.9M in 2020 from $276.3M in 2019

- 1.7 million learners spent on average $19 in 2020

- CorpU acquired for $30.4M — “payable in cash and stock”

- 83% of consumer course enrollments came from free courses

I think the first time I paid for an online course, it was on Udemy. Back in March 2013, in the early days of Class Central, when it was still a side project, I purchased a course called Raising Money for Startups (I’d link to it, but it no longer exists).

Now, Udemy is one of the biggest online education platforms. It has over 1,000 employees and is visited by 33 million people a month.

Back in January 2021, I compared Coursera and Udemy, anticipating that the two providers would go public in 2021. Two months later, Coursera went public. Now, it’s Udemy’s turn.

So I’ve done the same thing I did when Coursera filed to go public: I printed and read through the 230+ pages of Udemy’s Form S-1 or IPO prospectus. This is the third IPO prospectus I’ve read, the second being the one filed by Vancouver-based Thinkific, which went public on the Toronto Stock Exchange (TSX).

Udemy’s IPO filing finally gives us an opportunity to take a peek into the business and access details that private companies typically don’t share. And it also gives a clearer picture of the impact of the pandemic on Udemy, and by extension, on online education at large.

In a future article, I will compare the Coursera and Udemy businesses directly. But for now, let’s focus exclusively on Udemy’s business. It’s worth pointing out that I’m not going to evaluate Udemy as an investment opportunity. Finally, another disclaimer is that Class Central is an affiliate partner of Udemy.

Udemy Analysis

Right off the bat, I felt that Udemy’s IPO prospectus was a bit more cagey than Coursera’s. For instance, Coursera’s S-1 had financial details going back to 2017 while Udemy’s only goes back to 2019. (To learn more about Coursera’s IPO prospectus and all its nitty gritty details, head to our in-depth analysis.)

Overview

| 2019 | 2020 | Till June 2021 | |

| Total | $276.3m | $429.9m | $250.6m |

| Consumer | $225.5m | $326.4M | $171.8m |

| Business | $50.9m | $103.4m | $78.8m |

| Net Loss | ($69.7m) | ($77.6m) | ($29.3m) |

While reading through Udemy’s S-1, I came across a line that sounded familiar. I’d seen pretty much the same line in Coursera’s S-1, but phrased differently:

We have a history of losses, and we may not be able to generate sufficient revenue to achieve or maintain profitability in the future

As of June 30, 2021 the company has an accumulated deficit of $407.9 million. In 2020, Udemy made $430 million in revenue, 61% of which was outside of North America.

In 2020, 43% of our sales were denominated in currencies other than U.S. dollars, including euros, Indian rupees, British pounds sterling, Brazilian reais, and Japanese yen. Our expenses, by contrast, are primarily denominated in U.S. dollars.

According to Udemy’s prospectus, 73 million learners have registered on Udemy since its inception. But in their regular communications, the company generally mentions a lower number: 44 million learners (up from 10 million in 2017). Maybe these are the learners who have enrolled in at least one course or are active in a certain period of time.

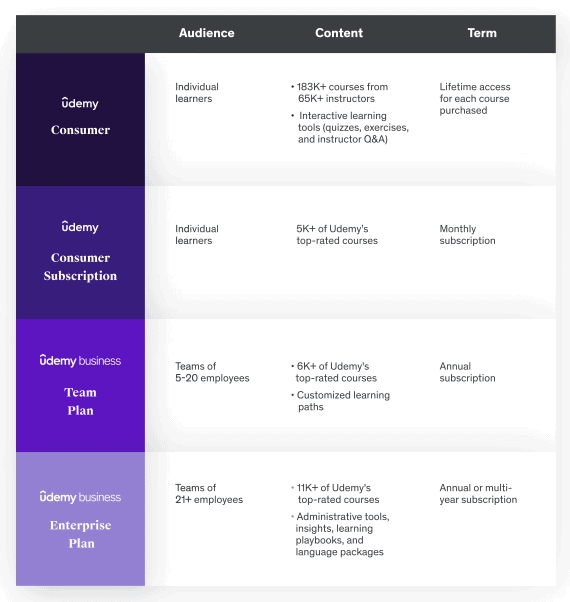

Udemy has two major business segments: Consumer and Udemy Business (UB).

Udemy Consumer

In Udemy’s consumer arm, there are two models.

In Udemy’s first model, learners can purchase a course outright and get lifetime access to it (in theory at least; I’ve noticed some of my older purchases no longer exist on the platform). Class Central analysis shows that the average listed price of a Udemy course is $71.3 while the median is $39.99. Course prices range from $19.99 to $199.99.

In their S-1, Udemy mentions:

For the years ended December 31, 2019 and 2020, we had 962 and 1,439 thousand monthly average buyers, respectively. For the six months ended June 30, 2020 and 2021, we had 1,521 and 1,364 thousand monthly average buyers, respectively.

Based on the consumer revenues, we can estimate that an average learner spent $19 in 2020 while they spent $21 in 2021 so far. Here’s what Udemy has to say about this increase:

For the six months ended June 30, 2021, total consumer revenue increased by $14.6 million, or 9%, compared to the same period in the prior year. The increase in consumer revenue was driven by a $10.5 million increase in revenue recognized in the period deferred from course purchases in the prior fiscal year. The remaining increase in consumer revenue was driven by an increase in the average purchase price of courses when compared to the same period in the prior year, partially offset by a 10% decrease in monthly average buyers

This shows that Udemy learners are very sensitive to pricing.

I think that out of the 15 Udemy courses I’ve purchased in the last eight years, I’ve only finished a couple. While the S-1 offers some numbers regarding cumulative learning (like 11 billion minutes of learning in 2020), it doesn’t mention completion rates.

But Udemy is well known for its deals, and many learners (if not all) purchase Udemy courses at a discount. Looking at my own purchase history, I’ve bought 15 Udemy courses since 2013, and the maximum I’ve paid for a single course is $19 (this was for the first course I bought).

Pricing is also different based on your location, and Udemy claims to apply machine learning algorithms.

Our ML pricing algorithms determine how much we charge for our courses in our marketplace on a per-country basis, taking into account dozens of course characteristics, including category of content, hours of content, course rating, and popularity.

In August, a class action suit was filed against Udemy in California related to its pricing practices. According to the class action lawsuit, Udemy engages in false reference pricing, which is when a seller fabricates a false “original” price for a product, then offers that product at a substantially lower price under the guise of a sale.

Back in June, my colleague @ruima wrote about six deceptive marketing practices from education companies in China, one of which was about advertising deceptive discounts.

Udemy’s second model is a new monthly subscription first reported by Class Central. It costs $30 per month and gives learners access to about 5000 courses (Udemy’s full catalog has over 170K courses). Unfortunately, Udemy didn’t share any numbers regarding subscriptions.

Udemy Business

The second segment, and the one that is growing much faster, is Udemy Business (UB). In this case, employers purchase annual subscriptions for their employees. These cost $360 a year for access to around 6000 courses of Udemy’s catalog.

As of December 31, 2019 and 2020, we had 5,174 and 7,300 UB customers, respectively. As of June 30, 2020 and 2021, we had 6,396 and 8,669 customers, respectively.

UB is contributing more and more to Udemy’s bottom line. In 2021 Q2, it accounted for a third of Udemy’s revenues.

In 2019 and 2020, 82% and 76%, respectively, of our revenue was derived from our consumer offering. For the six months ended June 30, 2020 and 2021, 78% and 69%, respectively, of our revenue was derived from our consumer offering.

Similar to Coursera for Business, UB is also more profitable for the company.

In 2020, content costs as a percentage of revenue were 42% for our consumer segment and 25% for our enterprise segment. In the six months ended June 30, 2021, content costs as a percentage of revenue were 39% for our consumer segment and 25% for our enterprise segment.

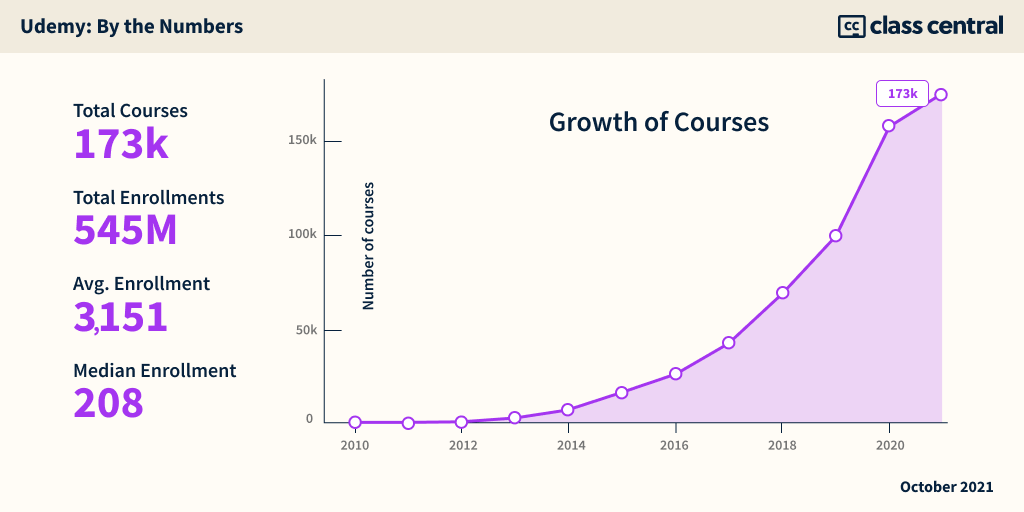

Udemy Catalog

Earlier this year, I also analyzed Udemy’s massive catalog of 157k courses. Here are some updated numbers collected from Udemy’s API:

| Total courses | 173K |

| Total enrollments (across catalog) | 545M |

| Average course enrollment | 3151 |

| Median course enrollment | 208 |

Officially, the numbers are a bit higher (since courses do get removed from the platform): 183k courses and 594 million enrollments. 83% of consumer enrollments came from free courses, resulting in 456 million cumulative free course enrollments.

But Class Central’s analysis shows that only 11% of the courses on Udemy’s platform are free. According to Udemy, over 3.7 million free learners have converted to buyers.

Udemy Instructors

| Instructor Payments | 2019 | 2020 | Till June 2021 |

| Total | $109.2m | $161.4M | $86.8M |

| Average | 2,950 | $1,574 | |

| >$1 k | 9,000+ | 6,000+ | |

| Top 5% | 71% | 70% |

Udemy has “relationships with over 65,000 instructors”. In 2020, these instructors earned $161.4M with an average of $2,950. 9000 of these earned over $1k in revenue.

Out of all these instructors, 5% generated 71% and 70% of paid marketplace enrollments during 2020 and the first half of 2021, respectively. Some back of the envelope calculations let us deduce that the top 3000 instructors made $3,500 on average in 2020.

Based on instructor registration records, Udemy estimates that a majority of their instructors are located outside the United States.

A shift towards subscriptions, be it in Udemy Business or Consumer segments, might lead to instructors revenues growing at a slower rate than Udemy’s.

CorpU Acquisition

At the end of August 2021, Udemy announced that it had acquired CorpU, which it described as “an online leadership development platform that delivers cohort-based immersive learning experiences and access to world-class experts”.

The acquisition price was $30 million.

On August 15, 2021, the Company entered into an Agreement and Plan of Merger (the “Merger Agreement”) with CUX (d/b/a CorpU), or CorpU, to acquire all outstanding shares of CorpU for approximately $30.4 million, payable in cash and 61,300 shares of Udemy restricted common stock.

Tags

Carla

I can’t find the consumer monthly subscription on udemy. Is it even live or did they pull that venture?

orcmid

On “My Udemy” if I pull down my profile, there is a Subscriptions entry. that is where I see the $29.99 monthly subscription, and the fact that I have no subscriptions.

orcmid

I notice that some instructors have flexed their Udemy courses into private organizations . These are often dual arrangements. The Udemy course is supported (and when a course is archived for some reason, the archive location is made available to current registrants).

I see this with highly-successful music courses and also game-development programming courses. An interesting hybrid arrangement is with ‘gamedev.tv’.

With regard to faux discounting, I tent to catch new courses at $9.99 discounted from over $100. That last one of those was a new course that had not been adequately “play-tested” and was a train-wreck for the intended beginner students. I can’t imagine anyone ever paying the supposed list price.

I’ve used MOOCs for as long as Coursera has been around. For Udemy, there are course quality issues and I have become watchful with regard to instructors who have misplaced their beginner mind somewhere in tacit understanding, no matter what their overall success has been.